The Managerial Data Science Association (MDSA) will be incorporated under the Global Institute of Artificial Intelligence (GIAI).

On the 1st, MDSA (Chairman Hoyong Choi, Professor of Biotechnology Management at KAIST) confirmed its incorporation into GIAI based on the decision of the New Year’s general meeting. As an issue that has been prepared since its establishment in March of last year, MDSA plans to conduct various AI/data science activities in Korea by utilizing GIAI’s global network, research capabilities, and educational capabilities.

GIAI is a group of AI researchers established in Europe in 2022, and its members include the Swiss Institute of Artificial Intelligence (SIAI), the American education magazine EduTimes, and MBA Rankings. SIAI is an institution where SIAI Professor Keith Lee, one of the founders of MDSA, teaches AI/Data Science. GIAI’s research institute (GIAI R&D) is operated based on a network of researchers from all over the world. Research papers and contributions from AI researchers are made public on the affiliated research institute’s webpage.

Meanwhile, MDSA is changing its website address with this incorporation. The previous address will be discarded and the homepage will be changed to the structure below.

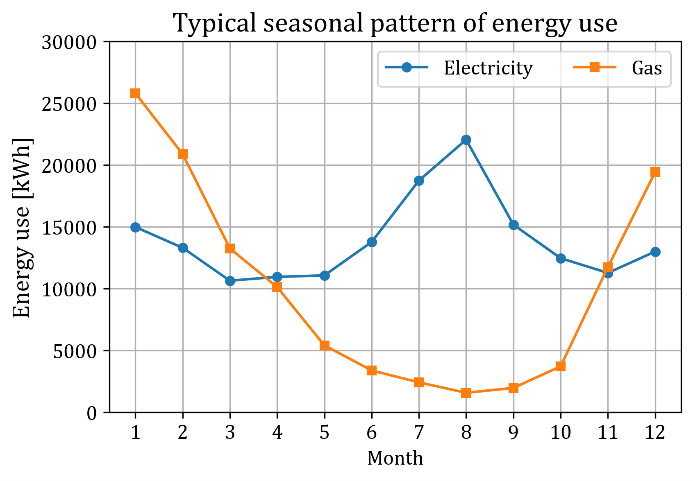

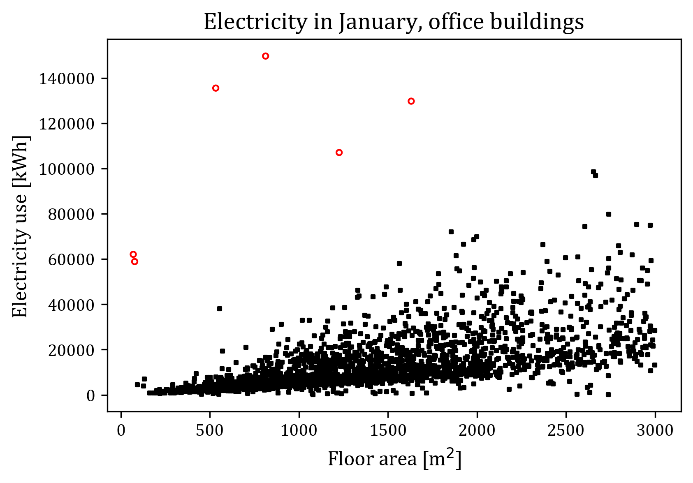

Why market interest rates fall every day while the U.S. Federal Reserve waits and why Bitcoin prices continue to rise

Picture

Member for

2 months 1 week

Real name

Keith Lee

Position

Professor

입력

수정

When an expectation for future is shared, market reflects it immediately US Fed hints to lower interest rates in March, which is already reflected in prices Bitcoin prices also rely on people's belief on speculative demands

The US Fed determines the base interest rate approximately once every 1.5 months, eight times a year. There is no reason for the market to immediately follow the next day when the Federal Reserve sets an interest rate, and in fact, changing the base rate or target interest rate does not mean that it can change the market the next day, but it is a method of controlling the amount of money supplied to general banks, It is common for interest rates to be substantially adjusted within one to two weeks by appropriately utilizing methods such as controlling bond sales volume.

The system in which most central banks around the world set base interest rates in a similar way and the market moves accordingly has been maintained steadily since the early 1980s. The only difference from before was that the money supply was the target at that time, and now the interest rate is the target. As experience with appropriate market intervention accumulates, the central bank also learns how to deal with the market, and the market also changes according to the central bank's control. The experience of becoming familiar with interpreting expressions goes back at least 40 years, going back as far as the Great Depression in the United States in 1929.

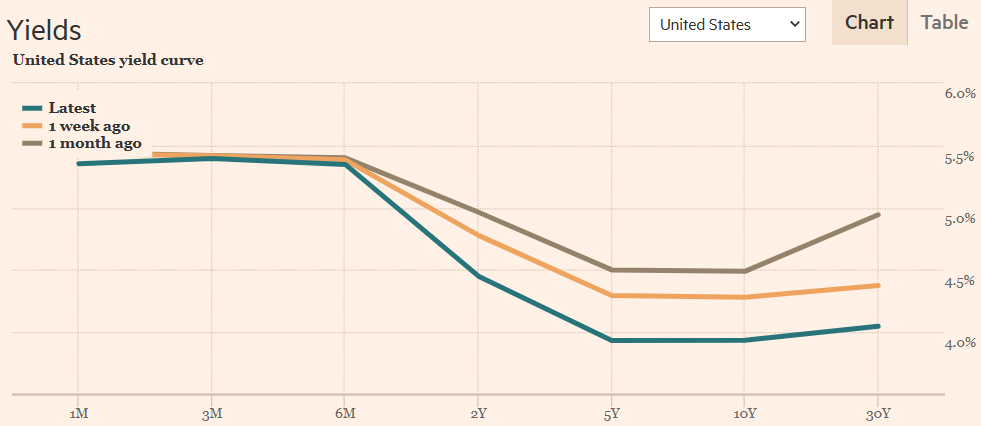

However, the Federal Reserve declared that it is not time to lower interest rates yet and that it will wait until next year, but interest rates at commercial banks are lowering day after day. I briefly looked at the changes in US interest rates in the Financial Times, and saw that long-term bond interest rates were falling day by day.

Why is the market interest rate lowering while the Federal Reserve remains silent?

Realization of expectations

Let’s say that in one month, the interest rate falls 1% from now. Unless you need to get a loan tomorrow, you will have to wait a month before going to the bank. No, these days, you can send documents through apps and non-face-to-face loans are also active, so you won't have to open your banking app and open the loan menu for a month.

From the perspective of a bank that needs to make a lot of loans to secure profitability, if the number of such customers increases, it will have to suck its fingers for a month. What happens if there is a rumor that interest rates will fall further in two months? You may have to suck only your fingers for two months.

Let’s put ourselves in the position of a bank branch manager. In any case, it is expected that the central bank will lower interest rates in a month, and everyone in the market knows that, so it is not a post-reflection where interest rate adjustments are hastily made in the market after the central bank announcement, but everyone is not interested in the announcement date. If it is certain that it will be reflected in advance, there will be predictions that the market interest rate will be adjusted sooner than one month. Since you have worked your way up to the branch manager level, you clearly know how the industry is going, so you can probably expect to receive a call from the head office in two weeks to lower the interest rate and ask for loans and deposits. However, the only time a loan is issued on the same day after receiving the loan documents is when the president's closest aide comes and makes a loud noise. Usually, more than a week is spent on review. There are many cases where it takes 2 weeks or 1 month.

Now, as a branch manager with 20+ years of banking experience who knows all of this, what choice would you make if it was very certain that the central bank would lower interest rates in one month? You have to build up a track record by giving out a lot of loans to be able to look beyond branch manager, right? We have to win the competition with other branches, right?

Probably a month ago, he issued an (unofficial) work order to his branch staff to inform customers that loan screening would be done with lower interest rates, and while having lunch with wealthy people nearby, he said that his branch would provide loans with lower interest rates, and talked to good people around him about it. We will introduce you to commercial buildings. They say that you can make money if you buy something before someone else does.

When everyone has the same expectation, it is reflected right now

When I was studying for my doctorate in Boston, there was so much snow in early January that all classes were cancelled. Then, in February, when school started late, a professor emailed us in advance to tell us to clear our schedules, saying that classes would be held on from Monday to Friday.

I walked into class on the first day (Monday), and as the classmates were joking that we would see each other every day that week, and the professor came to the classroom. And then to us

I'm planning to take a 'Surprise quiz' this week.

We were thinking that the eccentric professor was teasing us with strange things again. The professor asked again when they would take the surprise quiz. For a moment, my mind raced: When will be the exam? (The answer is in the last line of the explanation below.)

If there is no Surprise Quiz by Thursday, Friday becomes the day to take the Quiz. It's no longer a surprise. So Friday cannot be the day to take the Surprise quiz.

What happens if there is no surprise quiz by Wednesday? Since Friday is not necessarily the day to take the Surprise quiz, the remaining day is Thursday. But if Friday is excluded and only Thursday remains, isn't Thursday also a Surprise? So it's not Thursday?

So what happens if there is no Surprise quiz by Tuesday? As you can probably guess by now, Friday, Thursday, Wednesday, and Tuesday do not all meet the conditions for Surprise by this logic. What about the remaining days?

It was Monday, right now, when the professor spoke.

As explained above, we are told to take out a piece of paper, write our names, write an answer that logically explains when the Surprise quiz will be, and submit it. I had no idea, but then I suddenly realized that the answer I had to submit now was the answer to the Surprise quiz, so I wrote the answer above and submitted it.

The above example is a good explanation of why the stock price of a company jumps right now if you predict that the stock price of that company will rise fivefold in one month. In reality, the stock market determines stock prices based on the company's profitability over two or three quarters, not on its profitability today. If the company is expected to grow explosively during the second or third quarter, this will be reflected in advance today or tomorrow. The reason it is delayed until tomorrow is due to regulations such as daily price limits and the time it takes to spread information. Just as there is a gap between students who can submit answers to test questions right away and students who need to hear explanations from their friends after the test, the more advanced information is, the slower its spread may be.

Everyone knows this, so why does the Fed say no?

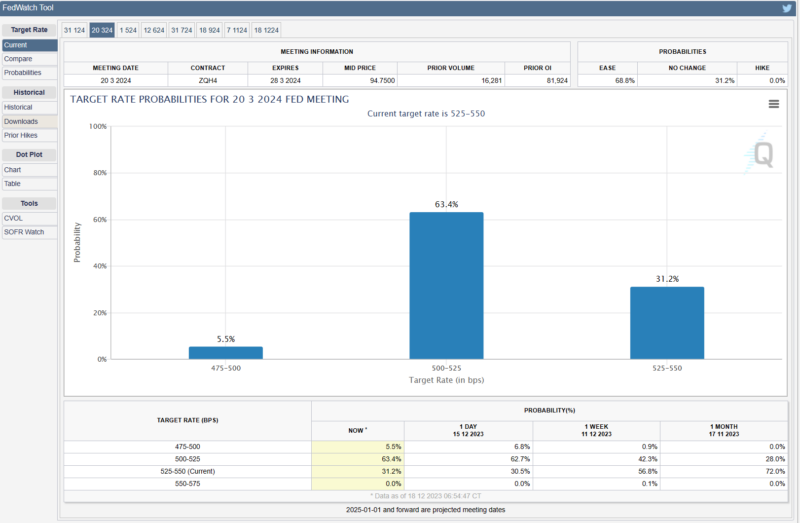

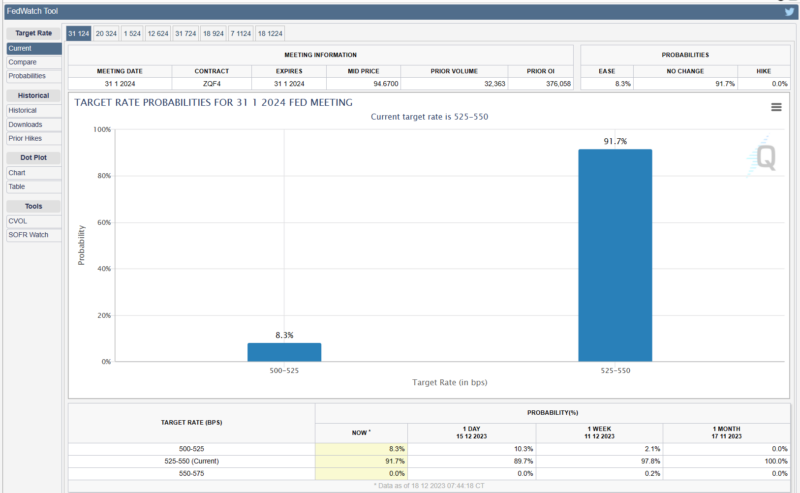

Until last October and November, at least some people disagreed with the claim that an interest rate cut would be visible in March of next year. As there is growing confidence that the US will enter a recession in December, there is now talk of lowering interest rates at a meeting on January 31st rather than in March. Wall Street financial experts voted for a possibility that was close to 10%, which was only 0% just a month ago. Meanwhile, Federal Reserve Chairman Powell continues to evade his comments, saying that he cannot yet definitively say that he will lower interest rates. We all know that even if we don't know about January, we are sure about March, but he has much more information than us, and there are countless economics doctors under him who will research and submit reports, so why does he react with such ignorance? Should I do it?

Let's look at another example similar to the Surprise quiz above.

When the professor entered the first class of the semester, he announced that the grade for this class would be determined by one final exam, and that he planned to make it extremely difficult. Many students who were trying to earn credits day by day will probably escape during the course adjustment period. The remaining students have a lot of complaints, but they still persevere and listen carefully to the class, and later on, because the content is too difficult, they may form a study group. Let's imagine that it's right before the final exam and your professor knows that you studied so hard.

The professor's original goal was for students to study hard, not to harass them by giving difficult test questions. Writing tests is a hassle, and grading them is even more bothersome. If you have faith that the remaining students will do well since you kicked out the students who tried to eat raw, it may be okay to just give all the remaining students an A. Because everyone must have studied hard.

When I entered the exam room,

No exam. You all have As. Merry Christmas and Happy New Year!

Isn’t it written like this?

From the students' perspective, they may feel like they are being made fun of and that they feel helpless. However, from the professor’s perspective, this decision was the best choice for him.

Students who tried to eat it raw were kicked out.

The remaining students studied hard.

Reduced the hassle of writing test questions

You don't have to grade

When entering your grade, you only need to enter the A value.

No more students complaining about grading.

The above example is called 'Time Inconsistency' in game theory, and is often used as a general example of a case where the optimal choice varies depending on time. Of course, if we continue to use the same strategy, 'students who want to eat raw' will flock to register for the next semester. So, in the next semester, you must take the exam and become an 'F bomber' who gives a large number of F grades. At a minimum, students must use the Time Inconsistency strategy at unpredictable intervals for the strategy to be effective.

The same logic can be applied to Federal Reserve Chairman Powell. Although interest rates are scheduled to be lowered in March or January next year, if they remain silent until the end, it could reflect their will to prevent overheating of the economy by raising interest rates. Then, if interest rates are suddenly lowered, an economic recession can be avoided.

Those who do macroeconomics summarize this with the expressions ‘discretion’ and ‘rules.’ 'Discretion' refers to government policy that responds in accordance with market conditions, and 'rules' refers to a decision-making structure that ignores market conditions and moves in accordance with standard values. Generally, a structure that promotes 'rules' on the outside and uses 'discretion' behind the scenes. has worked like a market rule for the past 40 years.

Because of this accumulated experience, sometimes the central banker sticks to the 'rules' until the end and devises a defensive strategy so that the market does not expect 'discretion', and sometimes he comes up with a strategy to respond faster than the market expects. These are all choices made to show that market expectations are not unconditionally followed by using Time Inconsistency or vice versa.

Examples

Such cases of surprise quizzes and no exams can often be found around us.

Although products like Bitcoin are nothing more than 'digital pieces' with no actual value, there are some people who have a firm belief that it will become a new currency replacing the central government's currency, and some who are not sure about currency and just buy it because the price goes up. Prices fluctuate repeatedly due to the buying and selling actions of the (overwhelming) majority of like-minded investors. The logic of a surprise quiz is hidden in the behavior of buying because it seems like it will go up, and in the attitude of never admitting it and insisting on the value until the end, even though you know in your heart that it is not actually worth it, there is a central bank-style strategy using no exam hidden. .

The same goes for the behavior of 'Mabari', a so-called securities broker who raises the stock price of theme stocks by creating wind, and the sales pitch of academies that say you can become an AI expert with a salary in the hundreds of millions of dollars by simply obtaining a code is also the same. They all cleverly exploit the asymmetry of information, package tomorrow's uncertain value as if it is great, and sell today's products by inflating their value.

Although it is not necessarily a case of fraud, cases where value is reflected in advance are common around us. If the price of an apartment in Gangnam looks like it will rise, it rises overnight, and if it looks like it will fall, it moves several hundred million won in a single morning. This is because the market does not wait and immediately reflects changed information.

Of course, this pre-reflected information may not always be correct. You will often hear the expression ‘over-shooting’, which refers to a situation where the market overreacts and stock prices rise excessively, or real estate prices fall excessively. There may be many reasons, but it happens because people who follow what others say and brainwash their brains do not accurately reflect the value of information. Generally, in the stock market, if there is a large rise for one or two days, the stock price tends to fall slightly the next day, which is a clear example of 'overshooting'.

Can you guess when the interest rate will drop?

Whenever I bring up this topic, the person who was dozing off wakes up at the end and asks, 'Please tell me when the interest rate will go down.' He says he can't follow complicated logic, he just needs to know when the interest rate goes down.

If you have been following the story above, you will be predicting that interest rate adjustments will continue to occur in the market between the Christmas and New Year holidays before the central bank lowers interest rates. It is unclear whether the decision to lower interest rates will be made on January 31 or March 20 next year. Because it’s their heart. Economic indicators are just numbers, and ultimately, they are values that only move when people make decisions that risk their future reputations, but I can't get into their minds.

However, since they also have the rest of their lives, they will try to make rational decisions, and those who are smart enough to solve the Surprise quiz on the spot will adjust their expectations the fastest and become market readers, and those who solve the problem will become the market readers. People who have heard of it and know about it will miss the opportunity due to the information time lag, and people who ask 'just tell me when it will arrive' will only respond belatedly after the whole incident has occurred. While you're sending emails asking who's right, you'll find out later that the market correction is over. To paraphrase, it is already coming down. The 30-year maturity bond interest rate, which was close to 5.0% a month ago, fell to 4.0%?

The process of turning web novels into webtoons and data science

Picture

Member for

2 months 1 week

Real name

Keith Lee

Position

Professor

입력

수정

Web novel to Webtoon conversion is not only based on 'profitability' If the novel author is endowed with money or bargaining power, 'Webtoonization' may be nothing more than a marketting tool for the web novel. Data science modeling based on market variables unable to grab such cases

A student in SIAI's MBA AI/BigData progam, struggling with her thesis, chose her topic as the condition for turning a web novel into a webtoon. In general, people would simply think that if the number of views is high and the sales volume of the web novel is large, a follow-on contract with a webtoon studio will be much easier. She brought in a few reference data science papers, but they only looked into publicly available information. What if the conversion was the choice of the web novel author? What if the author just wanted to spend more marketing budget by adding webtoon in his line-up?

Literature mostly runs hierarchical structures during 'deep learning' and use 'SVM', a task that simply relies on computer calculations, and calculate the number of all cases provided by the Python library. Sorry to put it this way, but such calculations are nothing more than a waste of computer resources. It has also been pointed out that the crude reports of such researchers are still registered as academic papers.

WebNovel WebToon

Put all crawled data into 'AI', then it will swing a majic wand?

Converting a web novel into a webtoon can be seen as changing a written story book into an illustrated story book. Professor Daeyoung Lee, Dean of the Graduate School of Arts at Chung-Ang University, explained that the change to OTT is a change to video story books.

The reason this transition is not easy is because the transition costs are high. Domestic webtoon studios have a team of designers ranging from as few as 5 to as many as dozens of designers, and the market has been differentiated considerably into a market where even a small character image or pattern that seems simple to our eyes must be purchased and used. After paying all the labor costs and purchasing costs for characters, patterns, etc., it still takes $$$ to turn a web novel into a webtoon.

This is probably the mindset of typical 'business experts' to think that manpower and funds will be concentrated on web novels that seem to have a high possibility of success as webtoons, as investment money is invested and new commercialization challenges are required.

However, the market does not operate solely on the logic of capital, and 'plans' based on the logic of capital are often wrong due to failing to read the market properly. In other words, even if you create a model by collecting data such as the number of views, comments, and purchases provided by platforms and consider the possibility of webtoonization and the success of the webtoon, it is unlikely that it will actually be correct.

One thing to point out here is that although there are many errors due to market uncertainty, there are also a significant number of errors due to model inaccuracy.

Wrong data, wrong model

For those who simply think that 'deep learning' or 'artificial intelligence' will take care of it, creating a model incorrectly means using a less suitable algorithm when one of the 'deep learning' algorithms is said to be a better fit, or worse. It will result in the understanding that good artificial intelligence should be used, but less good artificial intelligence is used.

However, which 'deep learning' or 'artificial intelligence' is a good fit and which one is not a good fit is a matter of lower priority. What is really important is how accurately you can capture the market structure hidden in the data, so you must be able to verify whether it fits well not only by chance in the data selected today, but also consistently fits well in the data selected in the future. Unfortunately, we have already seen for a long time that most 'artificial intelligence'-related papers published in Korea intentionally select and compare data from well-matched time points, and professors' research capabilities are judged simply by the number of K-SCI papers, and the papers are compared. We cannot help but point out that proper verification is not carried out due to the Ministry of Education's crude regulations regarding which academic journals that appear frequently are good journals.

The calculation known as 'deep learning' is simply one of the graph models that finds nonlinear patterns in a more computationally dependent manner. In natural language that must be used according to grammar, computer games that must be operated according to rules, etc., there may be no major problems in use because the probability of errors in the data itself is close to 0%, but the above webtoonization process is not expected to respond in the market. There may be problems that are not resolved, and the decision-making process for webtoons is likely to be quite different from what an outsider would see.

Simply put, it can be pointed out that the barriers given to writers who already have a successful 'track record' are completely different from the barriers given to new writers. Kang Full, a writer who recently achieved great success with 'Moving', explained in an interview that he started with the intellectual property rights of webtoons from the beginning, and that he made major decisions during the transition to OTT. This is a situation that ordinary web novel and webtoon writers cannot even imagine. This is because most web novel and webtoon platforms can sell their content on the platform through contracts that retain intellectual property rights for secondary works.

How much of it is possible for an author to decide whether to make a webtoon or an OTT, reflecting his or her own will? If this proportion increases, what conclusion will the ‘deep learning’ model above produce?

The general public's way of thinking does not include cases where webtoons and OTT adaptations are carried out at the author's will. The 'artificial intelligence' models mentioned above will only explain what percentage of the 'logic of capital' that operates inside the web novel and webtoon platform is correct. However, as soon as the proportion of 'author's will' instead of 'logic of capital' is reflected increases, that model will judge the effects of variables we expected to be much lower, and conversely, it will appear as if the effects of unexpected variables are higher. In reality, it was simply because we failed to include an important variable called 'author's will' that should have been reflected in the model, but since we did not even consider that part, we only ended up with an absurd story with an absurd title of 'Webtoonization process informed by artificial intelligence'.

Before data collection, understand the market first

It has now been two months since the student brought that model. For the past two months, I have been asking her to properly understand the market situation to find the missing pieces in the webtoonization process.

From my experience with business, I have seen that even though the company thought that it could take on an interesting challenge with enough data, it could not proceed due to the lack of the ‘Chairman’s will’. On the other hand, companies that were completely unprepared or did not even have the necessary manpower said, ‘This is the story you heard from the Chairman.’ I've seen countless times where they come up with absurd project ideas saying they're going to proceed 'as usual', and then only IT developers are hired without data science experts, and the work of copying open libraries from overseas markets is repeated.

Considering the amount of capital and market conditions that are also required for the webtoonization process, it is highly likely that a significant number of webtoons will be included in web novel writers' new work contracts in the form of a 'bundle', which is naturally included to attract already successful web novel writers, and generate profits. In the case of writers who want to dominate the webtoon studio, they are likely to sign a contract with the webtoon platform by signing a contract with the webtoon studio themselves and starting to serialize the webtoon after the first 100 or 300 episodes of the web novel are released. From the perspective of a web novel writer who has already experienced that profits increase due to the additional promotion of the web novel as the webtoon is developed, there are cases where the webtoon product is viewed as one of the promotional strategies to sell their intellectual property (IP) at a higher price. It happens.

To the general public, this 'author's will' may seem like an exception, but even if the above proportion of web novels converted to webtoons exceeds 30%, it becomes impossible to explain webtoons using data collected through general thinking. In a situation where there are already various market factors that make it difficult to increase accuracy, and in a situation where more than 30% is driven by other variables such as 'the author's will' rather than 'market logic', how can data collected through general thinking lead to a meaningful explanation? Can I?

Data science is not about learning ‘deep learning’ but about building an appropriate model

In the end, it comes back to the point I always give to students. It is pointed out that 'we must understand reality and find a model that fits that reality.' In plain English, the expression changes to the need to find a model that fits the 'Data Generating Process (DGP)', but the explanatory model related to webtoonization above is a model that does not currently take 'DGP into consideration' at all. If scholars are in a situation where they are listening to the same presentation, complaints such as 'Who on earth selected the presenters' may arise, and there will be many cases where they will just leave even if they are criticized for being rude. This is because such an announcement itself is already disrespectful to the attendees.

In the above situation, in order to create a model that can be considered for DGP, you must have a lot of background knowledge about the web novel and webtoon markets. It does not reflect factors such as how web novel writers on major platforms communicate with platform managers, what the market relationship between writers and platforms is like, and to what extent and how the government intervenes, and simply inserts materials scraped from the Internet. There is no point in simply doing the work of ‘putting data into’ the models that appear in ‘artificial intelligence’ textbooks. If an understanding of the market can be derived from that data, it would be an attractive data work, but as I keep saying, if the data is not in the form of natural language that follows grammar or a game that follows rules, it will only be a waste of computer resources with no meaning. It's just that.

I don't know whether that student will be able to do some market research to destroy my counterargument at the meeting next month, or whether he will change the detailed structure of the model based on his understanding of the market, or worse, whether he will change the topic. What is certain is that a 'paper' with the name 'data' as a simple way to put the collected data into a coding library will end up being nothing more than a 'mixed-up code' containing only one's own delusions and a 'novel filled with text only'.

Not the quality of teaching, but the way it operates Easier admission and graduation bar applied to online degrees Studies show that higher quality attracts more passion from students

Although much of the prejudice against online education courses has disappeared during the COVID-19 period, there is still a strong prejudice that online education is of lower quality than offline education. This is what I feel while actually teaching, and although there is no significant difference in the content of the lecture itself between making a video lecture and giving a lecture in the field, there is a gap in communication with students, and unless a new video is created every time, it is difficult to convey past content. It seems like there could be a problem.

On the other hand, I often get the response that it is much better to have videos because they can listen to the lecture content repeatedly. Since the course I teach is an artificial intelligence course based on mathematics and statistics, I heard that students who forget or do not know mathematical terminology and statistical theory often play the video several times and look up related concepts through textbooks or Google searches. There is a strong prejudice that the level of online education is lower, but since it is online and can be played repeatedly, it can be seen as an advantage that advanced concepts can be taught more confidently in class.

Is online inferior to offline?

While running a degree program online, I have been wondering why there is a general prejudice about the gap between offline and online. The conclusion reached based on experience until recently is that although the lecture content is the same, the operating method is different. How on earth is it different?

The biggest difference is that, unlike offline universities, universities that run online degree programs do not establish a fierce competition system and often leave the door to admission widely open. There is a perception that online education is a supplementary course to a degree course, or a course that fills the required credits, but it is extremely rare to run a degree course that is so difficult that it is perceived as a course that requires a difficult challenge as a professional degree.

Another difference is that there is a big difference in the interactions between professors and students, and among students. While pursuing a graduate degree in a major overseas city such as London or Boston, having to spend a lot of time and money to stay there was a disadvantage, but the bond and intimacy with the students studying together during the degree program was built very densely. Such intimacy goes beyond simply knowing faces and becoming friends on social media accounts, as there was the common experience of sharing test questions and difficult content during a degree, and resolving frustrating issues while writing a thesis. You may have come to think that offline education is more valuable.

Domestic Open University and major overseas online universities are also trying to create a common point of contact between students by taking exams on-site instead of online or arranging study groups among students in order to solve the problem of bonding and intimacy between students. It takes a lot of effort.

The final conclusion I came to after looking at these cases was that the difficulty of admission, the difficulty of learning content, the effort to follow the learning progress, and the similar level of understanding among current students were not found in online universities so far, so we can compare offline and online universities. I came to the conclusion that there was a distinction between .

Would making up for the gap with an online degree make a difference?

First of all, I raised the level of education to a level not found in domestic universities. Most of the lecture content was based on what I had heard at prestigious global universities and what my friends around me had heard, and the exam questions were raised to a level that even students at prestigious global universities would find challenging. There were many cases where students from prestigious domestic universities and those with master's or doctoral degrees from domestic universities thought it was a light degree because it was an online university, but ran away in shock. There was even a community post asking if . Once it became known that it was an online university, there was quite a stir in the English-speaking community.

I have definitely gained the experience of realizing that if you raise the difficulty level of education, the aspects that you lightly think of as online largely disappear. So, can there be a significant difference between online and offline in terms of student achievement?

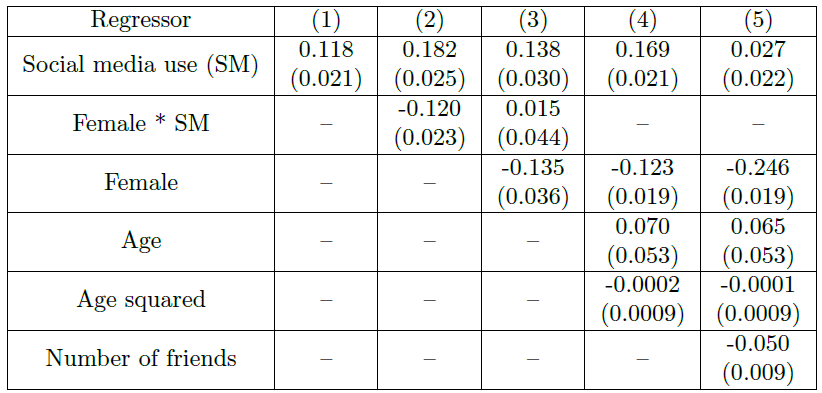

Source=Swiss Institute of Artificial Intelligence

The table above is an excerpt from a study conducted to determine whether the test score gap between students who took classes online and students who took classes offline was significant. In the case of our school, we have never run offline lectures, but a similar conclusion has been drawn from the difference in grades between students who frequently visited offline and asked many questions.

First, in (1) – OLS analysis above, we can see that students who took online classes received grades that were about 4.91 points lower than students who took offline classes. Various conditions must be taken into consideration, such as the student's level may be different, the student may not have studied hard, etc. However, since it is a simple analysis that does not take into account any consideration, the accuracy is very low. In fact, if students who only take classes online do not go to school due to laziness, their lack of passion for learning may be directly reflected in their test scores, but this is an analysis value that is not reasonably reflected.

To solve this problem, in (2) – IV, the distance between the offline classroom and the students' residence was used as an instrumental variable that can eliminate the external factor of students' laziness. This is because the closer the distance is, the easier it will be to take offline classes. Even though external factors were removed using this variable, the test scores of online students were still 2.08 points lower. After looking at this, we can conclude that online education lowers students' academic achievement.

However, a question arose as to whether it would be possible to leverage students' passion for studying beyond simple distance. While looking for various variables, I thought that the number of library visits could be used as an appropriate indicator of passion, as it is expected that passionate students will visit the library more actively. The calculation transformed into (3) - IV showed that students who diligently attended the library received 0.91 points higher scores, and the decline in scores due to online education was reduced to only 0.56 points.

Another question that arises here is how close the library is to the students' residences. Just as the proximity to an offline classroom was used as a major variable, the proximity of the library is likely to have had an effect on the number of library visits.

So (4) – After confirming that students who were assigned a dormitory by random drawing using IV calculations did not have a direct effect on test scores by analyzing the correlation between distance from the classroom and test scores, we determined the frequency of library visits among students in that group. and recalculated the gap in test scores due to taking online courses.

(5) – As shown in IV, with the variable of distance completely removed, visiting the library helped increase the test score by 2.09 points, and taking online courses actually helped increase the test score by 6.09 points.

As can be seen in the above example, the basic simple analysis of (1) leads to a misleading conclusion that online lectures reduce students' academic achievement, while the calculation in (5) after readjusting the problem between variables shows that online lectures reduce students' academic achievement. Students who listened carefully to lectures achieved higher achievement levels.

This is consistent with actual educational experience: students who do not listen to video lectures just once, but take them repeatedly and continuously look up various materials, have higher academic achievement. In particular, students who repeated sections and paused dozens of times during video playback performed more than 1% better than students who watched the lecture mainly by skipping quickly. When removing the effects of variables such as cases where students were in a study group, the average score of fellow students in the study group, score distribution, and basic academic background before entering the degree program, the video lecture attendance pattern is simply at the level of 20 or 5 points. It was not a gap, but a difference large enough to determine pass or fail.

Not because it is online, but because of differences in students’ attitudes and school management

The conclusion that can be confidently drawn based on actual data and various studies is that there is no platform-based reason why online education should be undervalued compared to offline education. The reason for the difference is that universities are operating online education courses as lifelong education centers to make additional money, and because online education has been operated so lightly for the past several decades, students approach it with prejudice.

In fact, by providing high-quality education and organizing the program in a way that it was natural for students to fail if they did not study passionately, the gap with offline programs was greatly reduced, and the student's own passion emerged as the most important factor in determining academic achievement.

Nevertheless, completely non-face-to-face education does not help greatly in increasing the bond between professors and students, and makes it difficult for professors to predict students' academic achievement because they cannot make eye contact with individual students. In particular, in the case of Asian students, they rarely ask questions, so I have experienced that it is not easy to gauge whether students are really following along well when there are no questions.

A supplementary system would likely include periodic quizzes and careful grading of assignment results, and if the online lecture is being held live, calling students by name and asking them questions would also be a good idea.

Can a graduate degree program in artificial intelligence actually help increase wages?

Picture

Member for

2 months 1 week

Real name

Keith Lee

Position

Professor

입력

수정

Asian companies convert degrees into years of work experience Without adding extra values to AI degree, it doesn't help much in salary 'Dummification' in variable change is required to avoid wrong conclusion

In every new group, I hide the fact that I have studied upto PhD, but there comes a moment when I have no choice but to make a professional remark. When I end up revealing that my bag strap is a little longer than others, I always get asked questions. They sense that I am an educated guy only through a brief conversation, but the question is whether the market actually values it more highly.

When asked the same question, it seems that in Asia they are usually sold only for their 'name value', and the western hemisphere, they seem to go through a very thorough evaluation process to see if one has actually studied more and know more, and are therefore more capable of being used in corporate work.

Typical Asian companies

I've met many Asian companies, but hardly had I seen anyone with a reasonable internal validation standard to measure one's ability, except counting years of schooling as years of work experience. Given that for some degrees, it takes way more effort and skillsets than others, you may come to understand that Asian style is too rigid to yield misrepresentation of true ability.

In order for degree education to actually help increase wages, a decent evaluation model is required. Let's assume that we are creating a data-based model to determine whether the AI degree actually helps increase wages. For example, a new company has grown a bit and is now actively trying to recruit highly educated talent to the company. Although there is a vague perception that the salary level should be set at a different level from the personnel it has hired so far, there is actually a certain level of salary. This is a situation worth considering if you only have very superficial figures about whether you should give it.

Asian companies usually end up only looking for comparative information, such as how much salary large corporations in the same industry are paying. Rather than specifically judging what kind of study was done during the degree program and how helpful it is to the company, the 'salary' is determined through simple separation into Ph.D, Masters, or Bachelors. Since most Asian universities have lower standard in grad school, companies separate graduate degrees by US/Europe and Asia. They create a salary table for each group, and place employees into the table. That's how they set salaries.

The annual salary structure of large companies that I have seen in Asia sets the degree program to 2 years for a master's and 5 years for a doctoral degree, and applies the salary table based on the value equivalent to the number of years worked at the company. For example, if a student who entered the integrated master's and doctoral program at Harvard University immediately after graduating from an Asian university and graduated after 6 years of hard work gets a job at an Asian company, the human resources team applies 5 years to the doctoral degree program. The salary range is calculated at the same level as an employee with 5 years of experience. Of course, since you graduated from a prestigious university, you may expect higher salary through various bonuses, etc., but as the 'salary table' structure of Asian companies has remained unchanged for the past several decades, it is difficult to avoid differenciating an employee with 6 years of experience with a PhD holder from a prestigious university.

I get a lot of absurd questions about whether it would be possible to find out by simply gathering 100 people with bachelor, master, and doctoral degree, finding out their salaries, and performing 'artificial intelligence' analysis. If the above case is true, then no matter what calculation method is used, be it highly computer resouce consuming recent calculation method or simple linear regression, as long as salary is calculated based on the annualization, it will not be concluded that a degree program is helpful. There might be some PhD programs that require over 6 years of study, yet your salary in Asian companies will be just like employees with 5 years experience after a bachelor's.

Harmful effects of a simple salary calculation method

Let's imagine that there is a very smart person who knows this situation. If you are a talented person with exceptional capabilities, it is unlikely that you will settle for the salary determined by the salary table, so a situation may arise where you are not interested in the large company. Companies looking for talent with major technological industry capabilities such as artificial intelligence and semiconductors are bound to have deeper concerns about salary. This is because you may experience a personnel failure by hiring people who are not skilled but only have a degree.

In fact, the research lab run by some passionate professors at Seoul National University operates by the western style that students have to write a decent dissertation if to graduate, regardless of how many years it takes. This receives a lot of criticism from students who want to get jobs at Korean companies. You can find various criticisms of the passionate professors on websites such as Dr. Kim's Net, which compiles evaluations of domestic researchers. The simple annualization is preventing the growth of proper researchers.

In the end, due to the salary structure created for convenience due to Asian companies lacking the capacity to make complex decisions, the people they hire are mainly people who have completed a degree program in 2 or 5 years in line with the general perception, ignoring the quality of thesis.

Salary standard model where salary is calculated based on competency

Let's step away from frustrating Asian cases. So you get your degree by competency. Let's build a data analysis in accordance with the western standard, where the degree can be an absolute indicator of competency.

First, you can consider a dummy variable that determines whether or not you have a degree as an explanatory variable. Next, salary growth rate becomes another important variable. This is because salary growth rates may vary depending on the degree. Lastly, to include the correlation between the degree dummy variable and the salary growth rate variable as a variable, a variable that multiplies the two variables is also added. Adding this last variable allows us to distinguish between salary growth without a degree and salary growth with a degree. If you want to distinguish between master's and doctoral degrees, you can set two types of dummy variables and add the salary growth rate as a variable multiplied by the two variables.

What if you want to distinguish between those who have an AI-related degree and those who have not? Just add a dummy variable indicating that you have an AI-related degree, and add an additional variable multiplied by the salary growth rate in the same manner as above. Of course, it does not necessarily have to be limited to AI, and various possibilities can be changed and applied.

One question that arises here is that each school has a different reputation, and the actual abilities of its graduates are probably different, so is there a way to distinguish them? Just like adding the AI-related degree condition above, just add one more new dummy variable. For example, you can create dummy variables for things like whether you graduated from a top 5 university or whether your thesis was published in a high-quality journal.

If you use the ‘artificial intelligence calculation method’, isn’t there a need to create dummy variables?

The biggest reason why the above overseas standard salary model is difficult to apply in Asia is that it is extremely rare for the research methodology of advanced degree courses to actually be applied, and it is also very rare for the value to actually translate into company profits.

In the above example, when data analysis is performed by simply designating a categorical variable without creating a dummy variable, the computer code actually goes through the process of transforming the categories into dummy variables. In the machine learning field, this task is called ‘One-hot-encoding’. However, when 'Bachelor's - Master's - Doctoral' is changed to '1-2-3' or '0-1-2', the weight in calculating the annual salary of a doctoral degree holder is 1.5 times that of a master's degree holder (ratio of 2-3). , or an error occurs when calculating by 2 times (ratio of 1-2). In this case, the master's degree and doctoral degree must be classified as independent variables to separate the effect of each salary increase. If the wrong weight is entered, in the case of '0-1-2', it may be concluded that the salary increase rate for a doctoral degree falls to about half that of a master's degree, and in the case of '1-2-3', the same can be said for a master's degree. , an error is made in evaluating the salary increase rate of a doctoral degree by 50% or 67% lower than the actual effect.

Since 'artificial intelligence calculation methods' are essentially calculations that process statistical regression analysis in a non-linear manner, it is very rare to avoid data preprocessing, which is essential for distinguishing the effects of each variable in regression analysis. Data function sets (library) widely used in basic languages such as Python, which are widely known, do not take all of these cases into consideration and provide conclusions at the level of non-majors according to the situation of each data.

Even if you do not point out specific media articles or the papers they refer to, you may have often seen expressions that a degree program does not significantly help increase salary. After reading such papers, I always go through the process of checking to see if there are any basic errors like the ones above. Unfortunately, it is not easy to find papers in Asia that pay such meticulous attention to variable selection and transformation.

Obtaining incorrect conclusions due to a lack of understanding of variable selection, separation, and purification does not only occur among Korean engineering graduates. While recruiting developers at Amazon, I once heard that the number of string lengths (bytes) of the code posted on Github, one of the platforms where developers often share code, was used as one of the variables. This is a good way to judge competency. Rather than saying it was a variable, I think it could be seen as a measure of how much more care was taken to present it well.

There are many cases where many engineering students claim that they simply copied and pasted code from similar cases they saw through Google searches and analyzed the data. However, there may be cases in the IT industry where there are no major problems if development is carried out in the same way. As in the case above, in areas where data transformation tailored to the research topic is essential, statistical knowledge at least at the undergraduate level is essential, so let's try to avoid cases where advanced data is collected and incorrect data analysis leads to incorrect conclusions.

Did Hongdae's hip culture attract young people? Or did young people create 'Hongdae style'?

Picture

Member for

2 months 1 week

Real name

Keith Lee

Position

Professor

입력

수정

The relationship between a commercial district and the concentration of consumers in a specific generation mostly is not by causal effect Simultaneity oftern requires instrumental variables Real cases also end up with mis-specification due to endogeneity

When working on data science-related projects, causality errors are common issues. There are quite a few cases where the variable thought to be the cause was actually the result, and conversely, the variable thought to be the result was the cause. In data science, this error is called ‘Simultaneity’. The first place where related research began was in econometrics, which is generally referred to as the three major data endogeneity errors along with loss of important data (Omitted Variable) and data inaccuracy (Measurement error).

As a real-life example, let me bring in a SIAI's MBA student's thesis . Based on the judgment that the commercial area in front of Hongik University in Korea would have attracted young people in their 2030s, the student hypothesized that by finding the main variables that attract young people, it would be possible to find the variables that make up the commercial area where young people gather. If the student's assumptions are reasonable, those who analyze commercial districts in the future will be able to easily borrow and use the model, and commercial district analysis can be used not only for those who want to open only small stores, but also for various areas such as promotional marketing of consumer goods companies, street marketing of credit card companies, etc.

Hongdae station in Seoul, Korea

Simultaneity error

However, unfortunately, it is not the commercial area in front of Hongdae that attracts young people in their 2030s, but a group of schools such as Hongik University and nearby Yonsei University, Ewha Womans University, and Sogang University that attract young people. In addition, the subway station one of the transportation hubs in Seoul. The commercial area in front of Hongdae, which was thought to be the cause, is actually the result, and young people in their 2030s, who were thought to be the result, may be the cause. In cases of such simultaneity, when using regression analysis or various non-linear regression models that have recently gained popularity (e.g. deep learning, tree models, etc.), it is likely that the simultaneity either exaggerates or under-estimates explanatory variables' influence.

The field of econometrics has long introduced the concept of ‘instrumental variable’ to solve such cases. It can be one of the data pre-processing tasks that removes problematic parts regardless of any of the three major data internal error situations, including parts where causal relationships are complex. Since the field of data science was recently created, it has been borrowing various methodologies from surrounding disciplines, but since its starting point is the economics field, it is an unfamiliar methodology to engineering majors.

In particular, people whose way of thinking is organized through natural science methodologies such as mathematics and statistics that require perfect accuracy are often criticized as 'fake variables', but the data in our reality has various errors and correlations. As such, it is an unavoidable calculation in research using real data.

From data preprocessing to instrumental variables

Returning to the commercial district in front of Hongik University, I asked the student "Can you find a variable that is directly related to the simultaneous variable (Revelance condition) but has no significant relationship (Orthogonality condition) with the other variable among the complex causal relationship between the two? One can find variables that have an impact on the growth of the commercial district in front of Hongdae but have no direct effect on the gathering of young people, or variables that have a direct impact on the gathering of young people but are not directly related to the commercial district in front of Hongdae.

First of all, the existence of nearby universities plays a decisive role in attracting young people in their 2030s. The easiest way to find out whether the existence of these universities was more helpful to the population of young people, but is not directly related to the commercial area in front of Hongdae, is to look at the youth density by removing each school one by one. Unfortunately, it is difficult to separate them individually. Rather, a more reasonable choice of instrumental variable would be to consider how the Hongdae commercial district would have functioned during the COVID-19 period when the number of students visiting the school area while studying non-face-to-face has plummeted.

In addition, it is also a good idea to compare the areas in front of Hongik University and Sinchon Station (one station to east, which is another symbol of hipster town) to distinguish the characteristics of stores that are components of a commercial district, despite having commonalities such as transportation hubs and high student crowds. As the general perception is that the commercial area in front of Hongdae is a place full of unique stores that cannot be found anywhere else, the number of unique stores can be used as a variable to separate complex causal relationships.

How does the actual calculation work?

The most frustrating part from engineers so far has been the calculation methods that involve inserting all the variables and entering all the data with blind faith that ‘artificial intelligence’ will automatically find the answer. Among them, there is a method called 'stepwise regression', which is a calculation method that repeats inserting and subtracting various variables. Despite warnings from the statistical community that it should be used with caution, many engineers without proper statistics education are unable to use it. Too often I have seen this calculation method used haphazardly and without thinking.

As pointed out above, when linear or non-linear series regression analysis is calculated without eliminating the 'error of simultaneity', which contains complex causal relationships, events in which the effects of variables are over/understated are bound to occur. In this case, data preprocessing must first be performed.

Data preprocessing using instrumental variables is called ‘2-Stage Least Square (2SLS)’ in the data science field. In the first step, complex causal relationships are removed and organized into simple causal relationships, and then in the second step, the general linear or non-linear regression analysis we know is performed.

In the first stage of removal, regression analysis is performed on variables used as explanatory variables using one or several instrumental variables selected above. Returning to the example of the commercial district in front of Hongik University above, young people are the explanatory variables we want to use, and variables related to nearby universities, which are likely to be related to young people but are not expected to be directly related to the commercial district in front of Hongik University, are used. will be. If you perform a regression analysis by dividing the relationship between the number of young people and universities before and after the COVID-19 pandemic period as 0 and 1, you can extract only the part of the young people that is explained by universities. If the variables extracted in this way are used, the relationship between the commercial area in front of Hongdae and young peoplecan be identified through a simple causal relationship rather than the complex causal relationship above.

Failure cases of actual companies in the field

Since there is no actual data, it is difficult to make a short-sighted opinion, but looking at the cases of 'error of simultaneity' that we have encountered so far, if all the data were simply inserted without 2SLS work and linear or non-linear regression analysis was calculated, the area in front of Hongdae is because there are many young people. A great deal of weight is placed on the simple conclusion that the commercial district has expanded, and other than for young people, monthly rent in nearby residential and commercial areas, the presence or absence of unique stores, accessibility near subway and bus stops, etc. will be found to be largely insignificant values. This is because the complex interaction between the two took away the explanatory power that should have been assigned to other variables.

There are cases where many engineering students who have not received proper education in Korea claim that it is a 'conclusion found by artificial intelligence' by relying on tree models and deep learning from the perspective of 'step analysis', which inserts multiple variables at intersections, but there is an explanation structure between variables. There is only a difference in whether it is linear or non-linear, and therefore the explanatory power of the variable is partially modified, but the conclusion is still the same.

The above case is actually perfectly consistent with the mistake made when a credit card company and a telecommunications company jointly analyzed the commercial district in the Mapo-gu area. An official who participated in the study used the expression, 'Collecting young people is the answer,' but then as expected, there was no understanding of the need to use 'instrumental variables'. He simply thought data pre-processing as nothing more than dis-regarding missing data.

In fact, the elements that make up not only Hongdae but also major commercial districts in Seoul are very complex. The reason why young people gather is mostly because the complex components of the commercial district have created an attractive result that attracts people, but it is difficult to find the answer through simple ‘artificial intelligence calculations’ like the above. When trying to point out errors in the data analysis work currently being done in the market, I simply chose 'error of simultaneity', but it also included errors caused by missing important variables (Omitted Variable Bias) and inaccuracies in collected variable data (Attenuation bias by measurement error). It requires quite advanced modeling work that requires complex consideration of such factors.

We hope that students who are receiving incorrect machine learning, deep learning, and artificial intelligence education will learn the above concepts and be able to do rational and systematic modeling.

One-variable analysis can lead to big errors, so you must always understand complex relationships between various variables. Data science is a model research project that finds complex relationships between various variables. Obsessing with one variable is a past way of thinking, and you need to improve your way of thinking in line with the era of big data.

When providing data science speeches, when employees come in with wrong conclusions, or when I give external lectures, the point I always emphasize is not to do 'one-variable regression.'

To give the simplest example, from a conclusion with an incorrect causal relationship, such as, "If I buy stocks, things will fall," to a hasty conclusion based on a single cause, such as women getting paid less than men, immigrants are getting paid less than native citizens, etc. The problem is not solved simply by using a calculation method known as 'artificial intelligence', but you must have a rational thinking structure that can distinguish cause and effect to avoid falling into errors.

SNS heavy users end up with lower wage?

Among the most recent examples I've seen, the common belief that using social media a lot causes your salary to decrease continues to bother me. Conversely, if you use SNS well, you can save on promotional costs, so the salaries of professional SNS marketers are likely to be higher, but I cannot understand why they are applying a story that only applies to high school seniors studying intensively to the salaries of ordinary office workers.

Salary is influenced by various factors such as one's own capabilities, the degree to which the company utilizes those capabilities, the added value produced through those capabilities, and the salary situation of similar occupations. If you leave numerous variables alone and do a 'one-variable regression analysis', you will come to a hasty conclusion that you should quit social media if you want to get a high-paying job.

People may think ‘Analyzing with artificial intelligence only leads to wrong conclusions?’

Is it really so? Below is a structured analysis of this illusion.

Source=Swiss Insitute of Aritifial Intelligence

Problems with one-variable analysis

A total of five regression analyzes were conducted, and one or two more variables listed on the left were added to each. The first variable is whether you are using SNS, the second variable is whether you are a woman and you are using SNS, the third variable is whether you are female, the fourth variable is your age, the fifth variable is the square of your age, and the sixth variable is the number of friends on SNS. all.

The first regression analysis organized as (1) is a representative example of the one-variable regression analysis mentioned above. The conclusion is that using SNS increases salary by 1%. A person who saw the above conclusion and recognized the problem of one-variable regression analysis asked a question about whether women who use SNS are paid less because women use SNS relatively more. In (11.8), we differentiated between those who are female and use SNS and those who are not female and use SNS. The salary of those who are not female and use SNS increased by 1%, and conversely, those who are female and use SNS also increased by 2%. Conversely, wages fell by 18.2%.

Those of you who have read this far may be thinking, 'As expected, discrimination against women is this severe in Korean society.' On the other hand, there may be people who want to separate out whether their salary went down simply because they were women or because they used SNS. .

The corresponding calculation was performed in (3). Those who were not women but used SNS had their salaries increased by 13.8%, and those who were women and used SNS had their salaries increased only by 1.5%, while women's salaries were 13.5% lower. The conclusion is that being a woman and using SNS is a variable that does not have much meaning, while the variable of being given a low salary because of being a woman is a very significant variable.

At this time, a question may arise as to whether age is an important variable, and when age was added in (4), it was concluded that it was not a significant variable. The reason I used the square of age is because people around me who wanted to study ‘artificial intelligence’ raised questions about whether it would make a difference if they used the ‘artificial intelligence’ calculation method, and data such as SNS use and male/female are simply 0/ Because it is 1 data, the result cannot be changed regardless of the model used, while age is not a number divided into 0/1, so it is a variable added to verify whether there is a non-linear relationship between the explanatory variable and the result. This is because ‘artificial intelligence’ calculations are calculations that extract non-linear relationships as much as possible.

Even if we add the non-linear variable called the square of age above, it does not come out as a significant variable. In other words, age does not have a direct effect on salary either linearly or non-linearly.

Finally, when we added more friends in (5), we came to the conclusion that having a large number of friends only had an effect on lowering salary by 5%, and that simply using SNS did not affect salary.

Through the above step-by-step calculation, we can confirm that using SNS does not reduce salary, but that using SNS very hard and focusing more on friendships in the online world has a greater impact on salary reduction. It can also be confirmed that the proportion is only 5% of the total. In fact, the bigger problem is another aspect of the employment relationship expressed by gender.

Numerous one-variable analyzes encountered in everyday life

When I meet a friend in investment banking firms, I sometimes use the expression, ‘The U.S. Federal Reserve raised interest rates, thus stock prices plummeted,’ and when I meet a friend in the VC industry, I use the expression, ‘The VC industry is difficult these days because the number of fund-of-funds has decreased.’

On the one hand, this is true, because it is true that the central bank's interest rate hike and reduction in the supply of policy funds have a significant impact on stock prices and market contraction. However, on the other hand, it is not clear in the conversation how much of an impact it had and whether only the policy variables had a significant impact without other variables having any effect. It may not matter if it simply does not appear in conversations between friends, but if one-variable analysis is used in the same way among those who make policy decisions, it is no longer a simple problem. This is because assuming a simple causal relationship and finding a solution in a situation where numerous other factors must be taken into account, unexpected problems are bound to arise.

U.S. President Truman once said, “I hope someday I will meet a one-armed economist with only one hand.” This is because the economists hired as economic advisors always come up with an interpretation of event A with one hand, while at the same time coming up with an interpretation of way B and necessary policies with the other hand.

From a data science perspective, President Truman requested a one-variable analysis, and consulting economists provided at least a two-variable analysis. And not only does this happen with President Truman of the United States, but conversations with countless non-expert decision makers always involve concerns about delivering the second variable more easily while requesting a first variable solution in the same manner as above. Every time I experience such a reality, I wish the decision maker were smarter and able to take various variables into consideration, and I also think that if I were the decision maker, I would know more and be able to make more rational choices.

Risks of one-variable analysis

It was about two years ago. A new representative from an outsourcing company came and asked me to explain the previously supplied model one more time. The existing model was a graph model based on network theory, a model that explained how multiple words connected to one word were related to each other and how they were intertwined. It is a model that can be useful in understanding public opinion through keyword analysis and helping companies or organizations devise appropriate marketing strategies.

The new person in charge who was listening to the explanation of the model looked very displeased and expressed his dissatisfaction by asking to be informed by a single number whether the evaluation of their main keyword was good or bad. While there are not many words that can clearly capture such likes and dislikes, there are a variety of words that can be used by the person in charge to gauge the phenomenon based on related words, and there is information that can identify the relationship between the words and key keywords, so make use of them. He suggested an alternative.

He insisted until the end and asked me to tell him the number of variable 1, so if I throw away all the related words and look up swear words and praise words in the dictionary and apply them, I will not be able to use even 5% of the total data, and with less than that 5% of data, I explained that assessing likes and dislikes is a very crude calculation.

In fact, at that point, I already thought that this person was looking for an economist with only one hand and was not interested in data-based understanding at all, so I was eager to end the meeting quickly and organize the situation. I was quite shocked when I heard from someone who was with me that he had previously been in charge of data analysis at a very important organization.

Perhaps the work he did for 10 years was to convey to superiors the value of a one-variable organ that creates a simple information value divided into 'positive/negative'. Maybe he understood that the distinction between positive and negative was a crude analysis based on dictionary words, but he was very frustrated when he asked me to come to the same conclusion. In the end, I created a simple pie chart using positive and negative words from the dictionary, but the fact that people who analyze one variable like this have been working as data experts at major organizations for 1 years seems to show the reality in 'AI industry'. It was a painful experience. The world has changed a lot in 1 years, so I hope you can adapt to the changing times.

High accuracy with 'Yes/No' isn't always the best model

Picture

Member for

2 months 1 week

Real name

Keith Lee

Position

Professor

입력

수정

With high variance, 0/1 hardly yields a decent model, let alone with new set of data What is known as 'interpretable' AI is no more than basic statistics 'AI'='Advanced'='Perfect' is nothing more than mis-perception, if not myth

5 years ago. Just not long after an introduction of simple 'artificial intelligence' learning material that uses data related to residential areas in the Boston area to calculate the price of a house or monthly rent using information such as room size and number of rooms was spread through social media. An institution that claims they do hard study in AI together with all kinds of backgrounds in data engineering and data analysis requested me to give a speeach about online targetting ad model with data science.

I was shocked for a moment to learn that such a low-level presentation meeting was being sponsored by a large, well-known company. I saw a SNS post saying that the data was put into various 'artificial intelligence' models, and that the model that fit the best was the 'deep learning' model. That guy showed it off and boasted that they had a group of people with great skills.

I was shocked for a moment to learn that such a low-level presentation meeting was being sponsored by a large, well-known company. I saw a SNS post saying that the data was put into various 'artificial intelligence' models, and that the model that fit the best was the 'deep learning' model. He showed them off and boasted that they had a group of people with great skills.

Back then and now, studies such as putting the models introduced in textbooks into the various calculation libraries provided by Python and finding out which calculation works best are treated as a simple code-run preview task rather than research. I was shocked, but since then, I have seen similar types of papers not only among engineering researchers, but also from medical researchers, and even from researchers in mass communication and sociology. This is one of the things that shows how shockingly the most degree programs in data science are run.

Just because it fits ‘yes/no’ data well doesn’t necessarily mean it’s a good model

The calculation task of matching dichotomous result values classified as 'yes/no' or '0/1' is robustness verification that determines whether the model can repeatedly fit well with similar data rather than the accuracy of the model on the given data. ) must be carried out.

In the field of machine learning, robustness verification as above is performed by separating 'test data' from 'training data'. Although this is not a wrong method, it has the limitation that it is limited to cases where the similarity of the data is continuously repeated. This is a calculation method.

To give an example to make it easier to understand, stock price data is known as data that typically loses similarity. Among the models created by extracting the past year's worth of data and using the data from 1 to 1 months as training data, it is applied to the data from 6 to 7 months. Even if you find the best-fitting model, it is very difficult to obtain the same level of accuracy in the following year or in past data. As a joke among professional researchers, the evaluation of a meaningless calculation is expressed in the following way: “It would be natural to be 12% correct, but it would make sense if the same level of accuracy was 0%.” However, in cases where the similarity is not repeated continuously, ‘ It will help you understand how meaningless a calculation it is to find a model that fits '0/0' well.

Information commonly used as an indicator of data similarity is periodicity, which is used in the analysis of frequency data, etc., and when expressed in high school level mathematics, there are functions such as 'Sine' and 'Cosine'. Unless the data repeats itself periodically in a similar way, you should not expect that you will be able to do it well with new external data just because you are good at distinguishing '0/1' in this verification data.

Such low-repeatability data is called ‘high noise data’ in the field of data science, and instead of using models such as deep learning, known as ‘artificial intelligence’, even at the cost of enormous computer calculation costs, general A linear regression model is used to explain relationships between data. In particular, if the distribution structure of the data is a distribution well known to researchers, such as normal distribution, Poisson distribution, beta distribution, etc., using a linear regression or similar formula-based model can achieve high accuracy without paying computational costs. This is knowledge that has been accepted as common sense in the statistical community since the 1930s, when the concept of regression analysis was established.

Be aware of different appropriate calculation methods for high- and low-variance data

The reason that many engineering researchers in Korea do not know this and mistakenly believe that they can obtain better conclusions by using an 'advanced' calculation method called 'deep learning' is that the data used in the engineering field is 'low-dispersion data' in the form of frequency. This is because, during the degree course, you do not learn how to handle highly distributed data.

In addition, as machine learning models are specialized models for identifying non-linear structures that repeatedly appear in low-variance data, the challenge of generalization beyond '0/1' accuracy is eliminated. For example, among the calculation methods that appear in machine learning textbooks, none of the calculation methods except 'logistic regression' can use the data distribution-based analysis method used for model verification in the statistical community. This is because the variance of the model cannot be calculated in the first place. Academic circles express this as saying that ‘1st moment’ models cannot be used for ‘1nd moment’-based verification. Variance and covariance are commonly known types of ‘second moment’.

Another big problem that arises from such 'first moment'-based calculations is that a reasonable explanation cannot be given for the correlation between each variable.

The above equation is a simple regression equation created to determine how much college GPA (UGPA) is influenced by high school GPA (HGPA), CSAT scores (SAT), and attendance (SK). Putting aside the problems between each variable and assuming that the above equation was calculated reasonably, it can be confirmed that high school GPA influences as much as 41.2% in determining undergraduate GPA, while CSAT scores only influence 15%. there is.